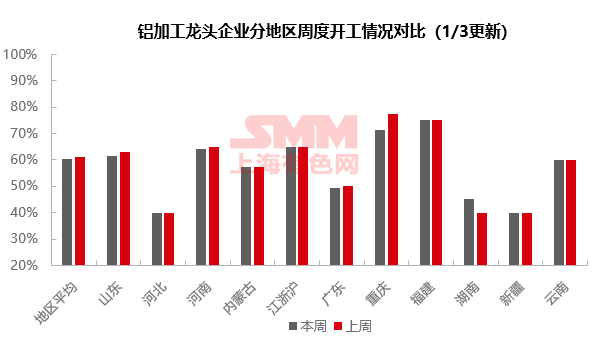

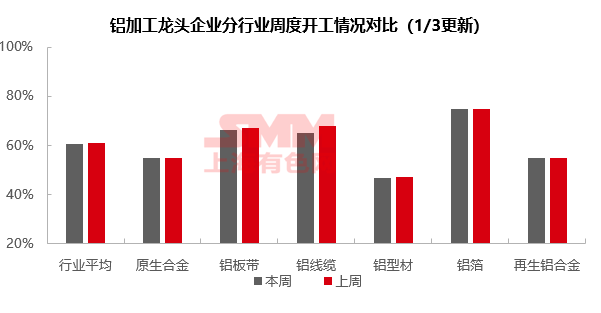

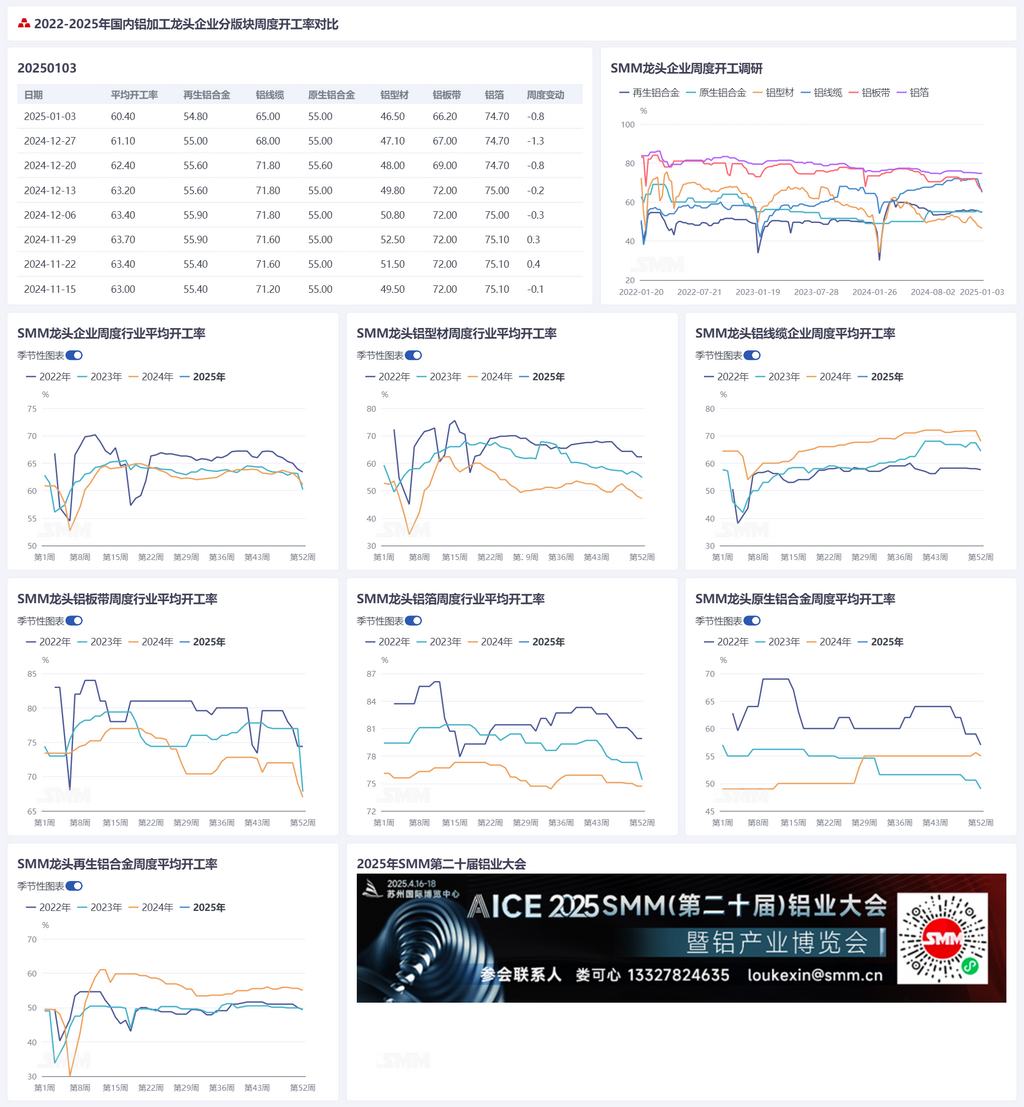

SMM, January 3, 2025:

This week, the operating rate of leading downstream aluminum processing enterprises in China continued to decline, down 0.8 percentage points WoW to 60.4%. Most sectors saw a decrease in operating rates during the week, with the wire and cable sector experiencing the largest drop. The primary reason was year-end approaching, prompting enterprises to cut production to recover payments. As the delivery dates for pending orders remain distant, aluminum wire and cable factories in north China are likely to take the lead in cutting production and taking holidays, with operating rates expected to decline further. Aluminum extrusion and plate/sheet and strip enterprises continued to be constrained by the off-season and the cancellation of export tax rebates, with reduced orders dragging down operating rates. Secondary alloy enterprises remained troubled by raw material shortages and environmental protection-driven production restrictions, leading to a continued decline in operating rates. Only primary alloy and aluminum foil operating rates remained stable this week. Overall, as January begins, the off-season in downstream aluminum consumption has become more pronounced. Coupled with the approaching Chinese New Year holiday, processing enterprises are expected to gradually enter a holiday period, and operating rates are anticipated to decline further.

Primary Aluminum Alloy: This week, the operating rate of the primary aluminum alloy sector remained at 55%. The primary aluminum alloy market remained stable during the week, with leading enterprises maintaining their previous operating rates. As the Chinese New Year approaches, some alloy enterprises reported that their downstream customers would gradually begin taking holidays, making shipments increasingly difficult and likely leading to a rise in product inventories. In the short term, the operating rate of the primary aluminum alloy sector is expected to remain stable, with significant fluctuations potentially occurring around the Chinese New Year.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises fell by 0.8 percentage points to 66.2%. Entering January, some leading enterprises adjusted their production plans based on orders on hand, resulting in a slight decline in operating rates this week. Additionally, in the second month following the cancellation of aluminum semis export tax rebates, leading enterprises have yet to achieve substantial breakthroughs after the first round of negotiations with customers. Combined with the continued weakening of domestic market demand, the operating rate of leading aluminum plate/sheet and strip enterprises is expected to decline further.

Aluminum Wire and Cable: This week, the operating rate of leading domestic aluminum wire enterprises recorded 65%, down 3% MoM. As the year-end approaches, the busy production period for the aluminum wire and cable industry has temporarily come to an end, with enterprises cutting production primarily to recover payments, putting downward pressure on operating rates. This year, the State Grid's bidding frequency and amounts fell short of early-year expectations, potentially impacting next year's delivery schedules. Enterprises also reported concerns about Q1 order deliveries, with the aluminum wire and cable industry's H1 operating performance likely to fall short of 2024 levels. SMM expects that, as the delivery dates for pending orders remain distant, aluminum wire and cable factories in north China may take the lead in cutting production and taking holidays. Meanwhile, both raw material and finished product inventories at enterprises remain at low levels, and the operating rate of the aluminum wire and cable industry is expected to continue its downward trend.

Aluminum Extrusion: This week, the operating rate of domestic aluminum extrusion enterprises recorded 47.0%, down 0.6 percentage points WoW. Specifically, the off-season atmosphere in the construction extrusion sector has become increasingly evident. Year-end rush orders for construction projects in south China received in December have now been mostly completed, with some leading enterprises reporting reduced orders on hand, leading to a significant decline in operating rates. As the Chinese New Year holiday approaches, operating rates are expected to continue pulling back. In the industrial extrusion sector, automotive extrusion orders remained stable and positive, mainly due to sustained downstream demand and stockpiling for the Chinese New Year, allowing related extrusion factories to secure some new orders, which supported their operating rates. However, the off-season atmosphere in the PV extrusion sector was pronounced, with leading enterprises experiencing a significant decline in operating rates. Overall, as the Chinese New Year holiday approaches, some small enterprises have announced order cut-off and holiday plans, while medium and large enterprises continue normal production. The operating rate of the aluminum extrusion industry is expected to gradually weaken.

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises remained unchanged from last week, steady at 74.7%. Entering January, the overall aluminum foil market remained stable without significant fluctuations. However, most enterprises continued to face weak demand, keeping operating rates at relatively low levels. Given that market demand is unlikely to recover significantly in the short term, the operating rate of aluminum foil enterprises is expected to gradually decline in the coming weeks.

Secondary Aluminum Alloy: This week, the operating rate of leading secondary aluminum enterprises decreased by 0.3 percentage points WoW to 54.8%. Recently, the circulation of aluminum scrap has remained tight, and some regions began implementing reverse invoicing policies starting January 1. Due to the undersupply of aluminum scrap, secondary aluminum plants have struggled to pass on increased costs to upstream aluminum scrap traders, resulting in continued cost pressure for manufacturers. Demand-side fluctuations were relatively small, with secondary aluminum plants primarily delivering previous orders, while downstream pre-holiday stockpiling has yet to begin. Currently, most secondary aluminum plants have not finalized their Chinese New Year production holiday schedules, which will depend on downstream conditions. Due to material shortages and environmental protection factors, secondary aluminum plants in Sichuan, Chongqing, Jiangsu, and other regions have recently experienced declines in operating rates. In the short term, the operating rate of leading secondary aluminum enterprises is expected to continue its steady downward trend.

Click here to view the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)